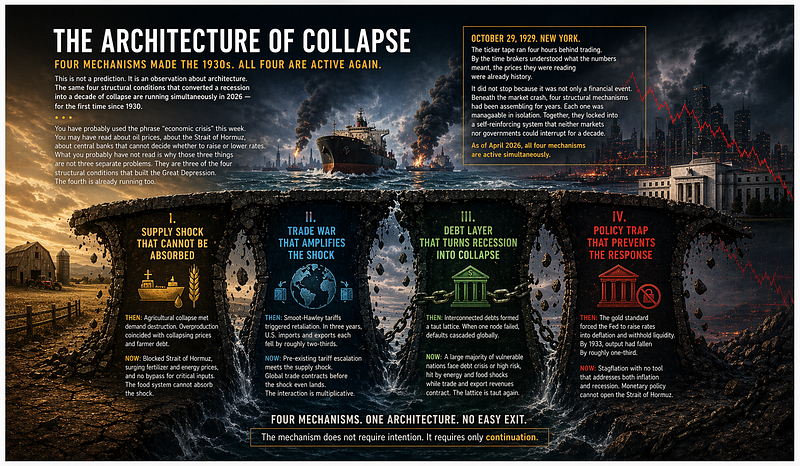

This is not a prediction. It is an observation about architecture. The same four structural conditions that converted a recession into a decade of collapse are running simultaneously in 2026 for the first time since 1930.

You have probably used the phrase “economic crisis” this week. You may have read about oil prices, about the Strait of Hormuz, about central banks that cannot decide whether to raise or lower rates. What you probably have not read is why those three things are not three separate problems. They are three of the four structural conditions that built the Great Depression. The fourth is already running too.

October 29, 1929. New York. The ticker tape ran four hours behind trading. By the time brokers understood what the numbers meant, the prices they were reading were already history.

It did not stop because it was not only a financial event. Four structural mechanisms had been assembling for years. Each one was manageable in isolation. Together, they locked into a self-reinforcing system that neither markets nor governments could interrupt for a decade.

Economists call it the Great Depression. The more precise description is: a collision of four mechanisms, none of which anyone stopped in time.

As of April 2026, all four mechanisms are active simultaneously.

I. The Supply Shock That Cannot Be Absorbed

In the 1920s, American farms overproduced to feed a recovering Europe. When demand fell, the debt farmers had taken on did not. By 1929, rural America was already in crisis before Wall Street registered a single decline. When the financial crash arrived, it landed on a system at breaking point. The supply glut and the demand collapse arrived together.

In 2026, the supply shock is physical rather than financial. On March 4, tanker traffic through the Strait of Hormuz collapsed within days of the strikes on Iran. Through that channel had passed a fifth of global oil consumption, nearly half of globally traded urea fertilizer, a significant share of LNG trade, and a third of the world’s helium supply. The bypass infrastructure handles roughly a quarter of normal flow, for oil only. For LNG, fertilizer, and helium, there is no bypass.

A blocked strait is not a headline. It is a machine that stops other machines.

This is the critical distinction from 2008. The financial crisis was a demand shock, money disappeared but physical production was intact. The 2026 shock is physical. No monetary policy instrument addresses a blocked maritime chokepoint.

II. The Trade War That Amplifies the Shock

In June 1930, President Herbert Hoover signed the Smoot-Hawley Tariff Act despite a petition from more than a thousand economists urging him not to. Retaliation was immediate. In the three years following enactment, American imports and exports each fell by roughly two-thirds. Smoot-Hawley did not cause the Depression. It caused the Depression to spread and deepen by destroying the system that had been absorbing it.

In April 2025 eleven months before the strikes on Iran the Peterson Institute for International Economics described the Trump tariff structure as the most sweeping American trade action in generations, explicitly comparable to the Smoot-Hawley era. Retaliation from China, the EU, and Canada followed within weeks.

In 1930, the tariff war arrived after the crash. In 2026, it arrived before the physical supply shock. The Hormuz blockade landed on a trading system already contracting. The interaction is not additive. It is multiplicative.

What made Smoot-Hawley catastrophic was not the tariffs. It was the moment: a system already under stress, with the distribution mechanism then removed.

Here is what changes when you see these not as two separate events but as one architecture: a supply shock needs a functioning trade system to distribute its costs. A trade war destroys exactly that system. When both run together, the cost has nowhere to go. It concentrates. And concentrated costs produce the third mechanism.

III. The Debt Layer That Turns Recession Into Collapse

The financial architecture beneath 1929 was a lattice of interconnected obligations. German reparations, British war debts, American bank loans to German businesses, Austrian banks holding German paper. When US banks called in loans, the chain pulled tight. The Credit-Anstalt bank in Vienna failed in May 1931. German banks followed. It was not greed or fraud. It was geometry: every node connected to every other, and the lattice was taut.

Debt does not collapse an order by itself. It collapses it when energy, trade, and policy all fail at once.

The IMF has assessed that a substantial majority of low- and middle-income countries are either already in debt crisis or at elevated risk, assessed before the Hormuz blockade. The blockade then imposed an energy and food price shock simultaneously on economies with no fiscal buffer, foreign-currency debt, and contracting export revenues. Egypt, Pakistan, Bangladesh, Sri Lanka, much of sub-Saharan Africa. More than a dozen nations have opened IMF emergency financing discussions.

The geometry is the same as 1931. In 1931, there was one Credit-Anstalt. In 2026, the number of nodes under simultaneous pressure is larger by an order of magnitude.

IV. The Policy Trap That Prevents the Response

After 1929, the Federal Reserve made what economists now consider the defining policy error of the twentieth century: it raised rates into a deflationary spiral and withheld liquidity as banks failed. The constraint was institutional, the gold standard. Franklin Roosevelt removed it in 1933. It was painful. It worked.

The 2026 trap is different in kind. Central bank tools were designed for three crisis categories: demand collapse, credit freeze, inflation surge. The 2026 shock belongs to none of them. It is a physical supply disruption across energy, fertilizer, semiconductor inputs, and pharmaceutical feedstocks, all flowing through a six-mile bottleneck.

Monetary tools can price panic. They cannot move a tanker.

In March 2026, Christine Lagarde and the ECB held rates unchanged while simultaneously raising the inflation forecast and cutting the growth projection, the precise combination for which no policy path was designed. Jerome Powell acknowledged the supply shock complicates the trajectory without offering a resolution.

An interest rate decision does not replant a fertilizer-starved field. The instrument that could address the 2026 mechanism is not monetary. It is diplomatic. And the core impasse a twenty-year uranium suspension demanded by Washington against a five-year offer from Tehran, has not moved since the Islamabad talks of April 11.

The Mechanism Does Not Require Intention

The Great Depression was not engineered. Herbert Hoover did not sign Smoot-Hawley to destroy international trade. The Federal Reserve did not raise rates to collapse the money supply. Each decision was made by people responding rationally to the pressures in front of them. The mechanisms interacted, and the system found a stable equilibrium at catastrophic depth before anyone understood what they were inside.

Note what the absence of an adequate intervention produces. Since February 28, the combined market capitalisation of America’s five largest defence contractors has increased by more than two hundred billion dollars. Vitol Group reported approximately two billion dollars in first-quarter profit. The institutional shareholders who hold simultaneous positions in defence, energy, and commodity infrastructure have no financial incentive to resolve the impasse faster than the market has priced.

The cascade has been modelled. It has not been stopped.

In 1930, the intervention that could have interrupted the cascade was monetary. It was available. For three years, it was not used. When Roosevelt finally used it, ten million Americans were unemployed.

In 2026, the intervention is diplomatic. It is available. Whether it will be used is a different question. One that is being answered, slowly, in the gap between twenty years and five.

The planting window has closed. The fertilizer is not coming back.

The mechanism does not require intention. It requires only continuation.

The Manifest Archive publishes two versions of each analysis. This is the condensed version. The full text including the complete debt geometry of the vulnerable economies, the three dimensions in which 2026 is structurally worse than 1930, and the full policy trap analysis is available on Substack. Free to read.

Related from The Manifest Archive