Type the question into a search bar and the answer arrives almost too quickly. The Federal Reserve, the institution that sets the price of money for the largest economy on earth, the body whose decisions move every mortgage, every currency, every government budget, is, according to the first result, owned by no one at all. The Federal Reserve System was created by an act of Congress in 1913, signed by Woodrow Wilson two days before Christmas, and it is, the central bank itself explains, not "owned" by anyone. The regional banks that make up the system do have shareholders, the commercial banks of each district, which are required by law to hold stock equal to six percent of their capital and surplus, only half of it ever actually paid in. But that stock cannot be sold, cannot be traded, cannot be borrowed against, and carries no control. In 2021 the Fed sent the United States Treasury roughly a hundred and seven billion dollars in profit. The richest, most powerful financial institution in the world hands its earnings to the government and answers, when asked who owns it, that the question does not apply.

All of that is true. Every clause of it is documented and correct. And it is one of the most elegant non-answers in the architecture of modern power, because it is accurate enough to end the conversation and empty enough to leave the real question untouched.

This essay is about that real question. Not who owns the Federal Reserve, which has a tidy and true answer, but what the tidy true answer is built to prevent you from asking next.

The official answer, and why it is technically true

Start by taking the institution at its word, because the word is honest as far as it goes.

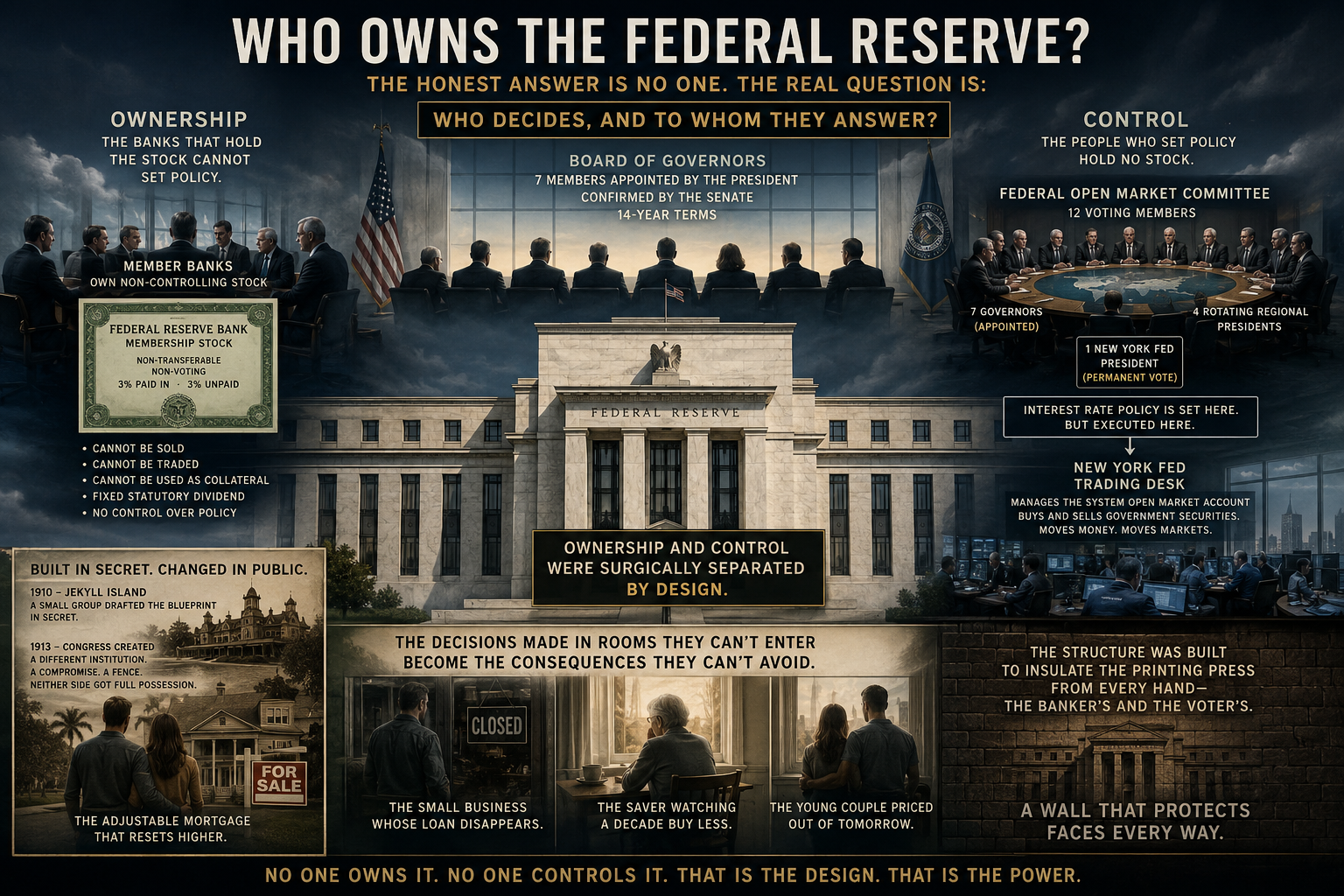

The Federal Reserve System has three parts, and they belong to different worlds. At the center sits the Board of Governors, in Washington, a federal government agency in the plainest sense: seven members, each nominated by the President and confirmed by the Senate, each serving a single fourteen-year term so long that no one President can appoint them all. The Chair, currently Kevin Warsh, who replaced Jerome Powell in 2026, serves a renewable four-year term laid over the longer one. This part of the Fed is as governmental as the Department of Justice. No private hand appoints a governor.

Around that federal core sit the twelve regional Federal Reserve Banks, in New York, Chicago, San Francisco and nine other cities, and these are stranger animals. They were deliberately built to look like private corporations. Each has shareholders. Each has a nine-member board of directors. Each turns what looks like a profit. And the shareholders are exactly the entities a conspiracy-minded reader expects: the commercial banks of the district, the JPMorgans and the community lenders alike, which the law requires to buy stock in their regional Reserve Bank as a condition of membership.

So far this sounds like ownership. It is the next set of facts that hollows the word out. The stock a member bank must hold cannot be sold to anyone. It cannot be traded on any market. It cannot be pledged as collateral for a loan. Only half of the required subscription is ever actually paid in, the other half a standing obligation the Fed has never once called. It pays a dividend fixed by statute, historically six percent, and since a 2015 law, for the largest banks, the lesser of six percent or the yield on a ten-year Treasury note, a number set by Congress, not by the bank's performance. And it confers no control over monetary policy whatsoever. A bank that holds this stock cannot vote on interest rates, cannot direct the institution, cannot do any of the things a shareholder in an ordinary company can do. The St. Louis Fed puts it plainly: holding this stock is nothing like owning shares in a public company. It is a membership fee dressed in the costume of equity.

This is why the official answer is true. In every sense that the word ownership normally carries, the right to sell, the right to control, the right to the residual profit, no one owns the Federal Reserve. The member banks hold a certificate that looks like a share and behaves like a license plate. The government appoints the governors but does not own the institution either; it receives the profit but does not direct the daily decisions. The Fed floats in a category built specifically for it, neither public nor private, owned by no one, and it floats there on purpose.

Hold that phrase, on purpose, because it is the whole of the matter. Most of what the Manifest examines is an architecture that emerged without an architect, a structure no one designed and everyone maintains. The Federal Reserve is the rarer thing. It is a structure that was designed, precisely, to be unownable. And a structure built to be unownable is built to answer one question, who owns it, so cleanly that you never reach the question it was actually built to settle.

Who actually owns the Federal Reserve Banks

Walk one step closer to the thing people are really asking when they type the question, which is not a legal question about share certificates but a suspicion: that the banks own the institution that is supposed to regulate them.

That suspicion is not stupid. The structure invites it. The regional Reserve Banks really are capitalized by the private banks of their districts. The boards of those regional banks really do include bankers: of the nine directors, three, the Class A directors, are elected by the member banks to represent the member banks. The other six are split between directors elected by the banks to represent the public and directors appointed by the Board of Governors in Washington, and the chair of each regional board must come from that last, public-appointed group. After the 2010 Dodd-Frank reforms, the banker-directors were barred from the one decision that most looked like a conflict, the selection of their regional bank's president, which is now made by the public-representing directors and must be approved by the federal Board in Washington.

So the honest picture is neither the official brochure nor the conspiracy. The private banks are inside the structure. They hold its peculiar stock, they elect a third of each regional board, they sit close to the machinery. And they are fenced, at every point where their presence would convert into control, by a federal layer that they do not appoint and cannot overrule. They own a seat in the room and not the decision made in it. The architecture lets the banker into the building and then removes, one by one, every lever he might reach for.

This is the second reason the ownership question dead-ends. The reader who suspects bank capture is closer to the truth than the reader who accepts the brochure, because the banks are genuinely woven in. But woven in is not the same as in command, and the gap between those two is exactly the space the structure was engineered to hold open. You can prove the banks are present. You cannot, from the ownership facts, prove they decide. And so the question that felt like it would end in a smoking gun ends instead in a diagram of offsetting committees, which is the most disappointing kind of answer and, here, the accurate one.

No, the Rothschilds do not own the Federal Reserve

There is a point in almost every search on this subject where the results turn, and a particular answer waits there, and it has to be addressed directly rather than stepped around.

The answer is a list. It circulates endlessly: a roster of supposed secret owners of the Federal Reserve, the Rothschild banks of London and Berlin, Lazard, Warburg, a handful of old European houses, presented as the hidden shareholders who really collect the money and pull the strings. It is worth saying clearly, because precision is the only thing that separates this essay from that one: the list is false. It is not a contested interpretation. It is fabricated. The named banks do not hold the stock; the stock is held by American member banks in each district, and several of the houses on the list were not members of the New York Fed at all. Fact-checkers across the spectrum have traced the list to nothing. In its most common form, the one that fixes on the Rothschilds, it is also one of the oldest antisemitic tropes in circulation, the secret Jewish financier behind the visible government, and it should be named as that and set down.

But notice why the list is so durable, because the reason is the actual subject of this piece. The fabricated answer thrives in the empty space that the true answer leaves behind. When the official reply to who owns this thing is no one, a reply that is accurate and final and somehow weightless, it leaves a vacuum precisely where a person's intuition insists something must be. The intuition is not wrong that power sits here. It is only wrong about the shape of it. The conspiracy supplies a shape, a name, a family, a hand, because a hand is easier to hold in the mind than a structure. The lie answers a real question that the true facts decline to engage. That is the recurring pattern of this whole domain: the documented truth is so carefully bounded that it abandons the field to the fabrication, and the fabrication wins not because it is believed over the evidence but because it is the only thing offering to answer the question the reader actually asked.

So we will give the real question its answer, and the answer is not a name. It is a design.

Who controls the Federal Reserve, then

If ownership is the wrong tool, switch tools. Stop asking who owns the Federal Reserve and ask who controls it, because control is where the power actually lives, and watch the answer scatter the moment you reach for it.

Monetary policy, the setting of interest rates that is the Fed's real instrument, is made by a body called the Federal Open Market Committee. It has twelve voting members. Seven are the federally appointed governors. One is always the president of the New York Fed, the regional bank that runs the actual buying and selling of government bonds. The remaining four seats rotate, year by year, among the presidents of the other eleven regional banks, so that a voting chair belongs to Cleveland one year and Dallas the next. Around the table sit the non-voting regional presidents too, speaking but not deciding. The decision that moves the world economy is made by a committee whose membership is part federal appointee, part rotating regional banker, assembled fresh each year, chaired by a presidential nominee who can be outvoted.

Try to locate the control inside that and it slips between your fingers. The President appoints the governors, but cannot set the rate, and cannot, in the ordinary reading of the law, even fire a governor he dislikes; the statute lets him remove one only "for cause," a phrase that has long been understood to mean misconduct, not disagreement. Congress created the Fed and can abolish or rewrite it, but does not run it and has deliberately held itself at arm's length. The member banks elect directors but not policy. The regional presidents vote but only some of them, only sometimes. Each actor holds a piece shaped so that it cannot be assembled with the others into a single will. The control has been deliberately broken into parts and the parts handed to people with different masters, different terms of office, different cities, different incentives, so that no one of them, and no clean coalition of them, can simply decide.

This is the chiasmus at the heart of the institution, and it is worth stating as flatly as it deserves: the people who own it do not control it, and the people who control it do not own it. The banks that hold the stock cannot set the rate. The governors who set the rate hold no stock. Ownership and control, which in a normal company are two names for the same thing, have here been surgically separated and housed in different bodies, and the separation is not a loophole or an accident. It is the entire mechanism.

Where the decision becomes an act

A committee that votes on interest rates has, by itself, changed nothing. A vote is a sentence. Somebody still has to make the money move, and the place where that happens is worth seeing, because it is the one point in the whole diffuse structure where the abstraction becomes a hand on a lever.

When the Federal Open Market Committee decides to lower or raise rates, it does not touch the rate directly; there is no dial in a vault. It issues a directive, and the directive travels to a single trading floor at the Federal Reserve Bank of New York, the desk that manages what is called the System Open Market Account. There, traders buy and sell government securities in enormous volume, adding money to the banking system or draining it out, until the rate at which banks lend to one another settles where the committee wanted it. This is why the New York Fed alone, of the twelve regional banks, holds a permanent vote on the committee: it is the bank that has to carry out what the committee decides. The decision is made by a rotating, federally anchored committee in Washington. The execution lives at one bank in lower Manhattan, a few hundred yards from the institutions whose cost of money it is setting.

Notice what this does to the ownership question one more time. The single most operationally powerful node in the system, the desk that actually moves the money, sits inside a regional Reserve Bank that is, on paper, capitalized by private member banks. If ownership were control, this is where it would surface. And it is precisely here that the structure is most carefully fenced: the New York Fed's president, who oversees the desk, is selected by the public-representing directors and approved by the federal Board in Washington, and the desk acts only on the committee's directive, never on its own initiative and never on its shareholders'. The place where the private banks stand physically closest to the lever is the place where the rules most thoroughly forbid them from touching it. Even at the operational heart of the system, ownership and control are held apart.

Who created the Federal Reserve, and how

To see why a thing was built this strangely, look at who built it, and at the night that the suspicious reader is, for once, partly right to be suspicious about.

In November 1910, a small group of men boarded a private rail car under conditions of real secrecy and traveled to a millionaires' retreat called the Jekyll Island Club, off the coast of Georgia. They had agreed to use only first names so the staff would not recognize them, and they let it be understood that they were a duck-hunting party. They were not. Around the table were Senator Nelson Aldrich, the most powerful financial legislator of his day; a senior Treasury official, A. Piatt Andrew; and three bankers who together represented the commanding heights of American finance, Henry Davison of the House of Morgan, Frank Vanderlip of National City Bank, the forerunner of Citibank, and Paul Warburg of Kuhn, Loeb and Company. Over about a week, in secret, they drafted the blueprint for a American central bank. The plan that emerged, the Aldrich Plan, was the direct ancestor of the Federal Reserve Act passed three years later.

The secrecy was not invented by later theorists. The participants admitted it themselves, eventually, with something close to pride. Frank Vanderlip wrote, a quarter century afterward, that he had been on that expedition "as secretive, indeed as furtive, as any conspirator." The man helped write the founding document of the system and called his own conduct furtive in print. The suspicious reader who senses that the Federal Reserve was born in a closed room among interested parties is, on the documented facts, correct.

And here is where the discipline matters, because the facts that vindicate the suspicion also bound it. The bankers at Jekyll Island drafted a plan. They did not enact one. The Aldrich Plan, openly associated with Wall Street, was politically toxic and failed. What Congress passed in 1913 was a substantially altered descendant of it, reshaped by a Democratic administration suspicious of exactly the men on that island, fitted with the federal Board of Governors that the bankers had not wanted, built so that the public layer sat on top of the private one rather than the reverse. The structure that resulted was not the bankers' wish granted. It was a compromise between the bankers' design and the political fear of the bankers, and the strange unownable shape of the modern Fed is the fossil of that compromise. The private banks got their decentralized regional banks; the public got a federal board to govern them; and the two were locked together in a way that gave neither full possession. The room was built by interested men, and then the thing built in the room was specifically arranged so that interested men could sit in it without owning it.

The determining variable is the structure, not the owner

Now the descent is complete, and the real variable is standing in plain view, and it was never an owner.

Ask who owns the Federal Reserve and the honest answer is no one, by design. Ask who controls it and the honest answer is no single body, by design. Both questions, the ownership question and the control question, run into the same wall, and the wall is the answer. The determining variable of this institution is not a person or a bank or a family. It is the structure of insulation itself: the deliberate arrangement by which the most consequential economic lever in the country was placed where neither private ownership nor public election can fully reach it. The Fed is not unowned because ownership is irrelevant to it. It is unowned because being unownable is the function. The thing the architecture produces, its actual output, is distance, distance between the setting of interest rates and anyone who could be made to answer for them at a shareholders' meeting or at the ballot box.

This is the inversion that the search-engine answer is built to hide. The official reply treats no one owns it as the reassuring end of the inquiry, the proof that there is nothing to see. Read correctly, it is the most important thing about the institution and the start of the real inquiry. An ordinary corporation can be bought, and so it can be captured by whoever buys it. A government agency can be voted out, and so it can be captured by whoever wins the election. The Federal Reserve was built to be neither, which means it was built to be capturable by no one, which sounds like a guarantee of safety until you turn it over and see the other face of the same fact: a thing that no one can capture is a thing that no one can command, including the public in whose name it acts. The insulation that keeps the banker's hand off the rate is the same insulation that keeps the voter's hand off it. You cannot build a wall that protects an institution from capture from one direction only. The wall faces every way at once.

So the compact form of the whole matter is this. When an institution cannot be owned, do not conclude that no power sits there. Ask instead what the structure was built to keep beyond everyone's reach, and who decided that it should be kept there, and what they removed from the ordinary world of ownership and votes in order to build it. The unownable institution is not the absence of a power question. It is a power question wearing the one disguise that makes people stop asking.

And the disguise is not neutral, because someone is served by it. The party that gains from no one owns it being accepted as the last word rather than the first question is the arrangement itself, whose autonomy lasts exactly as long as the public concludes there is nothing here to govern. Every actor in the structure has a quiet stake in the same blur: the member banks keep their dividend and their proximity without the scrutiny that visible control would invite, the governors keep a mandate that no election can revoke, and the politicians keep a place to send the blame for a hard economy they did not have to choose. The ambiguity is not a failure of explanation that better civics could fix. It is the structure protecting the one thing it cannot afford to have examined, which is its own distance from the vote.

What the structure was built to remove

Name precisely what was placed beyond reach, because the structure is not abstract, it took something specific out of the normal world and put it somewhere else.

What it removed is the control of the currency from the electoral cycle. In a democracy, almost everything that matters is, in principle, on the ballot. Tax rates, wars, borders, the size of the state, all of it can be argued about in an election and changed by one. The creation and pricing of money was deliberately lifted out of that arena and handed to appointees with fourteen-year terms specifically so that it could not be changed by an election, so that a President facing a hard campaign could not order cheap money into being to buy a good year, so that the thing every politician would most like to control would sit just past the edge of what any politician can. That is what the long terms are for. That is what the for-cause removal protection is for. That is what the whole unownable architecture is for. It is a fence around the printing press, and the fence is pointed inward at the government as much as outward at the banks.

And the distance is not abstract to the person standing on the far side of it. When the committee in Washington moves the rate, the effect arrives in a kitchen months later, unannounced and hard to trace: the adjustable mortgage that resets to a payment the family can no longer meet, the small business whose line of credit quietly doubles in cost, the saver watching a decade of careful balance buy a little less each month, the young couple priced out of a loan that was within reach the year before. None of them voted on it. None of them could. The decision that rearranged their month was taken in a room they have no door to, by people whose terms outlast the President they did vote for. That is what insulation feels like from below. Not protection from politics, but a cost that falls on you from a height you cannot petition.

And here the institution earns its strongest defense, which has to be stated at full strength rather than waved at, because it is the part of the argument that is genuinely on the Fed's side. The reason the printing press was fenced off from the vote is that the vote, turned loose on the printing press, has a terrible record. The textbook case sits in the 1970s, when an American President leaned on a compliant Fed chair to keep money loose into an election year, and the inflation that followed climbed into double digits and took a decade and a brutal recession to break. The man who broke it, raising rates until the economy buckled, could do so only because he was insulated, only because the structure let him do the savagely unpopular thing that no elected official facing voters could have survived doing. The case for the ownerless, unaccountable, insulated central bank is not a swindle. It is one of the more serious arguments in modern political economy, and it says: some levers are so dangerous in the hands of people who must win elections that the safest thing a democracy can do is build a room those people cannot enter, and put the lever in there.

That argument is real, and a piece that pretended otherwise would be committing the exact sin it is describing, ending the inquiry early because the convenient answer arrived. So let it stand at its full height. The insulation is defensible. The independence has prevented real harm. The fence around the printing press has, by the most cited reading of the record, saved the country from its own politicians more than once.

The test running right now

But a structure built to be beyond capture is only as real as the moment someone powerful tries to capture it, and that moment is happening as this is being written.

For all the decades that the Fed's independence was discussed as settled, the protection at its heart, the rule that a governor can be removed only "for cause" and not for disagreement, was rarely tested, because no President forced the question. That has changed. The current administration has moved to remove a sitting governor and has pressed the courts to confirm that it may, and the Supreme Court has begun to signal how it will treat the Fed's peculiar insulation when a determined President pushes against it. The outcome is not yet known, and this essay will not pretend to forecast it. What matters for the argument is only this: the determining variable, the structure of insulation, is not a permanent feature of the landscape. It is a legal arrangement, and legal arrangements hold exactly as long as the institutions around them agree to keep holding them. The wall that separates the printing press from the electoral cycle is being leaned on, deliberately, to find out whether it is masonry or paper.

This is what makes the ownership question worse than merely incomplete. While the country debates who owns the Federal Reserve, a question whose answer has not changed in a century, the thing that actually determines the Fed's power, whether its insulation survives contact with a President who refuses to respect it, is being decided almost without notice. The spotlight points at a settled question. The unsettled one moves in the dark. That is the signature of this entire field, and it is the reason the tidy answer is not harmless. A true answer that points attention away from the live question does the same work as a lie.

The honest case for an ownerless bank

Before the close, give the other side its turn in full, not as a courtesy but because the strongest version of the opposing case is the test of whether this argument is worth anything.

The defender of the Fed would say: you have described a problem and called it a scandal. Yes, the central bank is insulated from the vote. That is not a flaw the architects failed to notice; it is the achievement they were aiming at. Every advanced economy has arrived, by hard experience, at some version of the same answer, an independent monetary authority held at a distance from the politicians, because the alternative, money controlled directly by whoever just won power, produces the inflations that wreck currencies and the savings of ordinary people first. The unownable structure is not a trick to hide power from the public. It is a considered decision by the public's own representatives to bind themselves, the way a person hands the car keys to a friend before the party. The insulation is the binding. And the profits, the hundred billion in good years, flow not to any owner but straight to the Treasury, which is to say to the public; in recent years, when rising rates pushed the Fed into operating losses and it stopped sending money to the Treasury at all, no private owner made up the difference, because there is no private owner to make it up. An institution that hands its profits to the people and absorbs its losses for them is not owned in any sense that should alarm anyone.

This is a strong case. It is, on the economics, largely correct. And it does not touch the actual claim of this essay, which is narrower and harder to dismiss. The claim is not that central-bank independence is bad. The claim is that who owns the Federal Reserve is a question engineered to be answered in a way that forecloses the only debate that matters, which is whether, and how far, and answerable to whom, a sphere of public life should be placed permanently beyond public reach. The defender's case is precisely that debate, conducted honestly, and the ownership framing is what prevents most people from ever having it. You can believe, as serious people do, that the insulation is wise, and still see that no one owns it is not a reassurance but a description of the most important political decision embedded in the whole design. The disagreement between the Fed's defenders and its critics is a real and worthy one. The ownership question is the thing that keeps it from being had.

What you are actually asking

So return, at the end, to the search bar, and to the person typing the question, because the question was never naive.

They type who owns the Federal Reserve and the machine answers, correctly, no one, and the answer is meant to feel like a door closing. It should feel like a door opening. Behind it is not a secret list of families, which is a fairy tale, and not a simple agency of the government, which is a half-truth, but something stranger and more consequential than either: an institution deliberately constructed to belong to no one, so that the most powerful economic lever in the world could be held at a distance from every hand that might be made to answer for it, the banker's and the voter's alike. The people who own it do not control it, and the people who control it do not own it, and that severance is not the boring technicality the official answer presents. It is the design, the purpose, and the whole of the power.

You were never really asking who collects the dividend. You were asking who decides, and to whom they answer, and whether the most important room in the economy was built with a door the public can open. The honest answer to that question is not no one. The honest answer is that the door was bricked over on purpose, a long time ago, by men who left their names off the guest list, and that someone, right now, is testing whether the bricks still hold.

Frequently Asked Questions

Who owns the Federal Reserve?

No private individual or family. The Federal Reserve was created by Congress in 1913. Its regional banks have member commercial banks as shareholders, required to hold non-tradable stock that confers no control, and the Fed remits its profit to the US Treasury, roughly 107 billion dollars in 2021. Ownership is the wrong frame; control runs through the federal mandate.

Does a private bank or family own the Fed?

No. The member-bank stock cannot be sold, traded, or borrowed against, and carries no control. The myth of a secret private owner mistakes a legal technicality, the required shareholding, for control over policy.

Is the Federal Reserve private or public?

Both, by design. It is a federally created and overseen system, with a government-appointed Board, built on privately capitalized regional banks. It is a public-private hybrid answerable to Congress, not a private company.

Where do the Federal Reserve's profits go?

To the US Treasury. After expenses and the fixed statutory dividend, the Fed remits the remainder to the federal government, on the order of 107 billion dollars in 2021.

Evidence Map

Facts, interpretations, forecasts, and disconfirming signals.

Core claim. "Who owns the Federal Reserve?" is a question engineered to be answerable in a way that forecloses the real one. The honest answer (no one, by design) is true but weightless; the determining variable is not an owner but the STRUCTURE OF INSULATION that deliberately places monetary policy beyond both private ownership and electoral control. Ownership and control, fused in a normal company, were surgically separated: the banks that hold the stock cannot set policy, and the body that sets policy holds no stock.

Evidence level. Facts (high, documented): the Fed's three-part structure; member banks hold non-transferable, non-controlling stock equal to 6% of capital (3% paid in) at a statutory dividend; the FOMC's 12-vote composition; regional-bank governance (Class A/B/C, Dodd-Frank bar on banker-directors selecting presidents); ~$107B remitted to Treasury in 2021 and operating losses / suspended remittances since September 2022; the 1913 Act signed by Wilson; the 1910 Jekyll Island drafting meeting (Aldrich, A. Piatt Andrew, Davison, Vanderlip, Warburg) and Vanderlip's own "furtive as any conspirator" admission; the current "for cause" removal litigation. Interpretation (medium, marked): the reading that the structure's PURPOSE is insulation-from-the-vote and that the ownership framing functions to foreclose the real debate. Rejected/false (named): the "Rothschild / secret foreign owners" list is fabricated and, in its common form, an antisemitic trope.

What would confirm this. Continued evidence that no single actor can direct FOMC policy; that the "for cause" protection is invoked precisely to keep monetary policy beyond electoral reach; that public attention stays fixed on ownership while the insulation question is decided elsewhere.

What would disprove this. Evidence that member banks or any private owner can actually direct interest-rate policy (true ownership-control fusion); or that the structure offers no real insulation from electoral pressure and bends routinely to whoever holds the White House, which would make "insulation" the illusion rather than the design.

Watchlist. The Supreme Court's resolution of the "for cause" removal question and any reshaping of Fed independence; the size and duration of the Fed's deferred asset (suspended Treasury remittances); whether central-bank independence holds or erodes across advanced economies.

Related from The Manifest Archive

- Rothschild, the Federal Reserve, and BlackRock

- BlackRock, Vanguard and State Street: The Monopoly No One Designed

- Is the U.S. Dollar Losing Reserve Currency Status? The Quiet Erosion Explained

- The Rise of BRICS: The Second Rail Beneath the Dollar

- Who Decides What a Democracy Can Afford?

- The Ownership Illusion: License vs Ownership in the Digital Age

Jerry van der Laan writes The Manifest Archive, daily forensic essays on power, language, and the systems that shape what we are allowed to see as reality. He traces the structures beneath them.