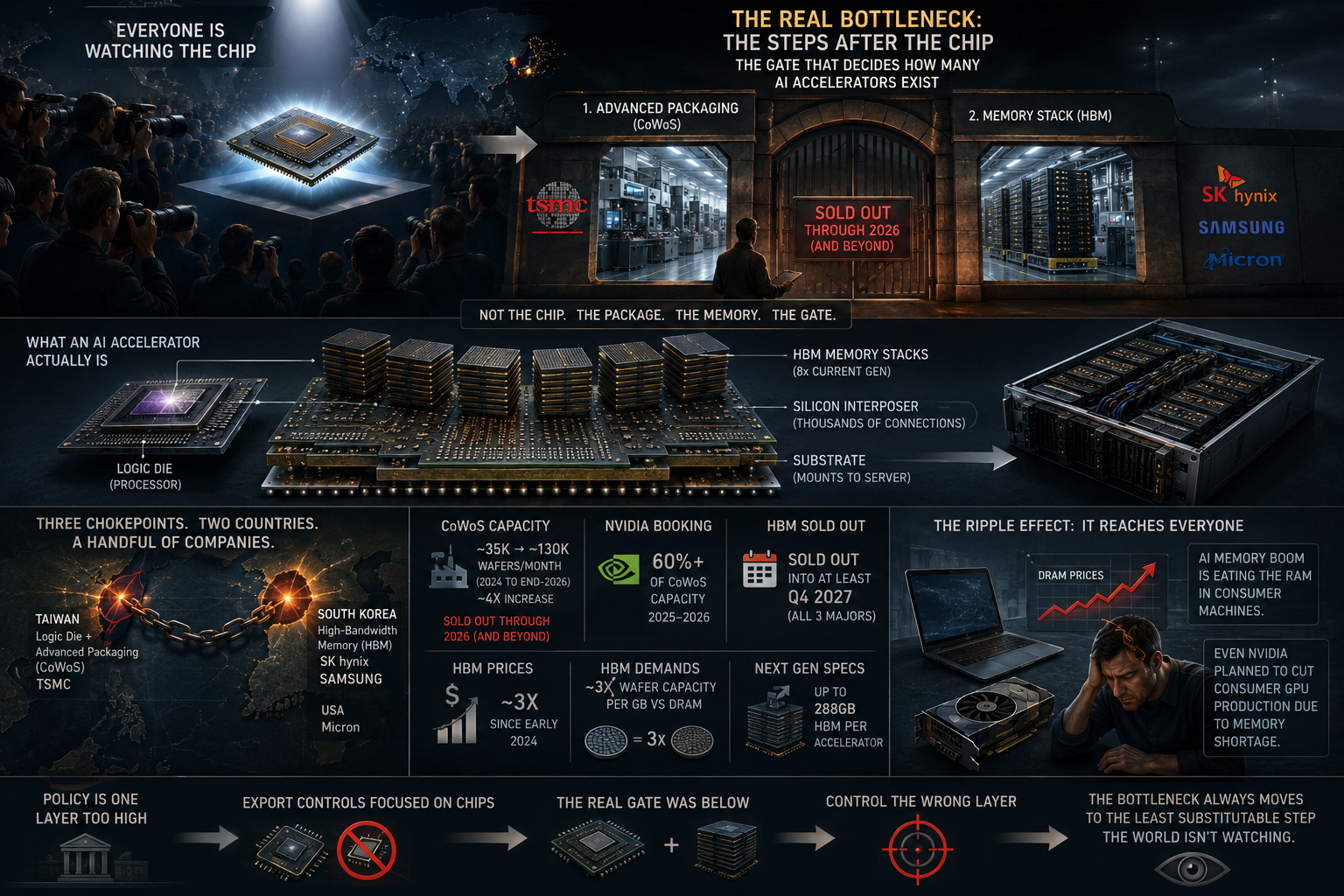

Everyone is watching the chips. The thing that actually decides how many AI accelerators exist is the step after the chip is made, and a memory stack built mostly in one country that is not the one everyone is watching.

For three years the whole world has fixed its attention on a single object: the chip. The AI race, the export controls, the trillion-dollar valuations, the anxiety about Taiwan, all of it organizes around the silicon logic die, the processor at the heart of an AI accelerator. Governments restrict it. Companies hoard it. Analysts count it. And the entire framing is one layer too high, because a fabricated logic die is not an AI chip. It is a component that cannot do anything, cannot ship, cannot compute, until it has been through two further steps that almost no one outside the industry can name.

The first is advanced packaging, the process that marries the logic die to its memory on a single piece of engineered silicon. The second is the memory itself, a specialized, brutally hard-to-make stack called high-bandwidth memory. These two steps, not the famous chip, are where the AI hardware boom is actually rationed. The determining variable in how much artificial intelligence the world can build is not the processor everyone watches. It is the packaging line and the memory stack that almost no one does. And because a single buyer can reserve that gate years in advance, the bottleneck does not only ration how much intelligence gets built. It decides who is allowed to build it.

The Chip Is Not the Bottleneck

Start with the thing people get wrong, because the whole analysis follows from correcting it. When you read that a company has "made" an AI chip, what has usually happened is that a logic die has been fabricated on a wafer, the famous front-end step performed at a few-nanometer node. That die is a marvel and it is also, on its own, inert. To become a working AI accelerator it must be joined to its high-bandwidth memory and mounted together on a substrate, in a back-end process the industry calls advanced packaging. Only after that does the object compute, and only after that can it ship.

This matters because the two steps scale at completely different rates. Front-end wafer fabrication, the part everyone talks about, has enormous installed capacity and a clear if expensive path to more. The back-end packaging and the memory are far more concentrated, far harder to expand, and far slower to build, and so as demand exploded the binding constraint quietly slid from the front end to the back end. By 2026 the chokepoint was no longer "can we make the dies." It was "can we package the dies we have already made," and the answer, repeatedly and on the record, was no. Even a perfectly fabricated logic die now sits and waits, because the step that turns it into a shippable product is full. The world is fabricating chips it cannot finish.

This is the first hidden gate, and it has a name that has never once appeared in a political speech: CoWoS.

What an Accelerator Actually Is

It helps to picture the object, because the picture is not what the word "chip" suggests. A modern AI accelerator is not a single square of silicon. It is an assembly. At its center sit one or more logic dies, the processors, and arranged around them sit several tall stacks of high-bandwidth memory, each stack itself a tower of memory chips bonded one on top of another. All of these are placed onto a silicon interposer, a flat engineered wafer that acts as an ultra-dense wiring board carrying the thousands of connections between the logic and the memory, and the whole thing is then mounted on a substrate to become the part that slots into a server. The current generation of flagship accelerators carries on the order of eight memory stacks around its logic; the next generation pushes the memory toward three hundred gigabytes per part.

Look at that object and the conventional framing inverts. By physical area, and increasingly by bill of materials, an AI accelerator is mostly memory and interposer, not processor. The logic die is the smallest and, in supply terms, the least scarce part of the thing named after it. The expensive, slow, sold-out parts are the memory stacks and the packaging that holds them together. We named the product after its rarest-sounding component and its least binding constraint, and then we spent three years regulating and counting that component while the actual scarcity lived in the parts we never learned to see.

CoWoS, the Gate Below the Chip

CoWoS stands for Chip-on-Wafer-on-Substrate, and it is the packaging technology, pioneered and dominated by TSMC, that assembles a high-end AI accelerator. It places the logic die and the memory stacks side by side on a silicon interposer, a tiny engineered platform that lets them communicate at the enormous speeds an AI workload demands, and then mounts the whole assembly on a substrate. Without it, the most advanced logic die in the world is a paperweight. With it, you have a Blackwell or a Rubin or an MI300. CoWoS is the difference between a chip and a product.

And it is sold out. TSMC executives, normally guarded, have said plainly that their CoWoS capacity is very tight and remains sold out through 2025 and into 2026. The company is expanding it at a pace that would be extraordinary in any other context, from roughly thirty-five thousand wafers a month in late 2024 toward a projected one hundred and thirty thousand a month by the end of 2026, close to a fourfold increase in under two years, and it is still not enough to meet demand. The chief executive of the dominant AI chip company said in early 2025 that advanced packaging capacity had quadrupled in two years and remained a bottleneck for his own firm. Quadrupled, and still short. That is what a real constraint looks like.

The concentration is the part that should focus the mind. A single company, Nvidia, has reportedly secured well over sixty percent of all of TSMC's CoWoS capacity for 2025 and 2026, locking up the majority of the world's advanced packaging the way a tenant might lease most of a building before anyone else can move in. Every other chip designer, the startups, the rivals, the cloud companies building their own silicon, competes for what is left. The entire visible drama of the AI chip race, who designs the best processor, is being quietly settled one layer down, by who controls the packaging line that turns any processor into a product. You can design the finest die on earth and ship nothing, because the gate is not the design. It is the assembly.

Why You Cannot Rush a Package

The natural response to a shortage is to ask why they do not simply build more, and advanced packaging is a near-perfect case study in why that question underestimates physical constraints. CoWoS is not a process you scale by flipping a switch. The interposers are large, in the most advanced versions larger than the standard reticle that defines how much a lithography tool can pattern at once, which pushes the process to the edge of what the equipment can do and holds yields below those of mature manufacturing. Every assembly is intricate, with thousands of microscopic connections that must all land correctly, and a failure late in the process throws away not just a cheap part but a fully fabricated logic die and a set of expensive memory stacks already mounted on it. The cost of a defect rises the further down the chain it occurs, and packaging is near the end of the chain.

Adding capacity means building cleanrooms, which take years, and filling them with specialized bonding and inspection equipment whose makers have their own backlogs, and then training the process to acceptable yield, which takes longer still. This is why even a fourfold expansion can remain sold out: the expansion was committed years ago against a demand forecast that the reality then blew past. It is the same path-dependency that governs every piece of heavy infrastructure. The decision that determines whether you have enough packaging in 2027 had to be made in 2024, before anyone knew how large the demand would become, and a decision not made early enough cannot be recovered by spending more later. Capacity at this layer is not bought. It is pre-committed, and the window to commit it closes long before the shortage it would have prevented becomes visible.

The Anchor Tenant

The concentration is not only geographic and technical. It is also commercial, and it compounds the constraint into something closer to a moat. When a single buyer secures well over half of the world's advanced-packaging capacity for years in advance, that buyer has done more than guarantee its own supply. It has converted the bottleneck into a barrier against everyone else. A rival can design a competitive processor, raise the capital, and book the wafers, and still find that the packaging slots required to turn that processor into a product are already spoken for. The gate is held not by the best design but by the deepest pre-commitment.

This is the quiet way dominance in AI hardware perpetuates itself, and it has little to do with the quality of the chip. The leader's advantage is increasingly that it got to the gate first and reserved it, so that the scarce step everyone depends on is, in practice, controlled by the incumbent who locked it up. Competition in design is fierce and visible; competition for the packaging line is the one that actually decides who can ship, and it was settled by contracts signed before most rivals knew the gate existed. You can out-design the leader and still not out-ship it, because the constraint that matters was claimed in advance. The bottleneck does not merely limit supply. It entrenches whoever was early enough to own it.

The Memory Wall

The second hidden gate is, if anything, harder, and it lives in a different country. An AI accelerator is not mostly logic. By area and increasingly by cost it is mostly memory, specifically high-bandwidth memory, or HBM, the stacked memory that feeds the processor data fast enough to keep it busy. A modern accelerator carries enormous quantities of it; the coming generation of Nvidia's hardware is specified with up to two hundred and eighty-eight gigabytes of next-generation HBM per chip. The processor is the brain, but the brain starves without the memory, and the memory is the harder thing to make.

HBM is sold out, and not for months but for years. SK Hynix, the South Korean company that makes roughly half the world's HBM, warned in late 2025 that its HBM was sold out years deep, into 2027, and Samsung and Micron, the only other two makers on earth, echoed the timeline. Three companies, two of them Korean, make essentially all of it, and all three are sold out for the better part of three years. The price has behaved accordingly, with HBM contract prices reported to have tripled since early 2024. This is not a market with slack. It is a market where the entire output is spoken for before it exists.

What makes HBM such a vicious constraint is a fact about its physics that ripples far beyond AI. Producing a given amount of HBM consumes something like three times the wafer capacity of ordinary DRAM, the normal computer memory, because the dies are smaller and the stacking is fiendishly complex. So every gigabyte of HBM the industry makes for AI is, in effect, three gigabytes of ordinary memory it did not make. The memory makers, rationally, are pouring their best capacity into the HBM that AI will pay almost anything for, and starving the ordinary DRAM market to do it. The bottleneck in an AI data center reaches all the way to the price of the memory in a laptop.

How the Bottleneck Moved

The migration of the constraint is recent enough to trace, and the sequence is the clearest evidence that the bottleneck is a moving thing rather than a fixed one. In the first phase of the boom, around 2023, the scarce thing genuinely was the leading-edge logic, the advanced wafers themselves, and the conversation about chips was, for that moment, correct. Then the front end caught up faster than the back end, and through 2024 the binding constraint slid to CoWoS: suddenly the dies existed but could not be packaged, and TSMC's advanced-packaging lines became the thing everyone was waiting on. Then, as packaging capacity began its enormous expansion, the constraint slid again, into memory, and by late 2025 and into 2026 the loudest shortage was HBM, sold out years deep, with the memory makers unable to expand fast enough and consumer memory dragged into the deficit behind it.

Three phases in three years, and in each phase the public conversation was describing the previous one. The chip framing that is correct for 2023 is wrong for 2026, and yet it persists, because the language of a constraint outlives the constraint itself. This is the temporal signature of a determining variable: it does not announce its move. It simply shifts to the next least-substitutable step while everyone is still fighting the last battle, and the only way to see it is to stop watching the object that was scarce last year and ask which step is sold out this year.

The Bottleneck Always Moves

Step back and a general law appears, one that reaches far past chips. In any complex production chain under sudden, enormous demand, the bottleneck migrates to the least substitutable step, and the public's attention arrives one full layer too late. People watched the logic die because the logic die was the last bottleneck, the constraint of the previous era, when designing a leading processor was the hard part. They kept watching it after the constraint had already moved beneath them to packaging and memory, because attention is sticky and the new gate is invisible and unpronounceable. The spotlight stayed on the chip. The chip started waiting on the package.

This is why the framing of the entire AI hardware debate is slightly and consequentially wrong. Export controls are written about "chips," and the chip is no longer the scarce thing. Headlines count processors, and the processors pile up unfinished for want of packaging slots and memory stacks. The strategic conversation is fighting the last bottleneck while the real one operates undisturbed one layer down, exactly the pattern that lets a determining variable do its work in plain sight. The breakthrough gets the attention. The bottleneck decides the outcome. And the bottleneck is always the step nobody has learned to name yet.

The Memory Supercycle

The HBM shortage is not an isolated event but the trigger of a broader upheaval the memory industry calls a supercycle, and the scale reframes how large this constraint really is. The market for high-bandwidth memory is projected to grow from roughly thirty-five billion dollars in 2025 toward a hundred billion by 2028, a pace that pulls the entire memory industry's investment, talent, and best capacity toward it. When a single component grows that fast and pays that well, every maker reorients around it, and everything that competes with it for the same factories gets squeezed.

That is why the AI memory shortage has become an everyone shortage. The same wafers and the same advanced production lines that could make ordinary memory are being redirected to the HBM that AI will pay almost anything for, and because HBM is so much more capacity-intensive per usable gigabyte, the redirection drains the ordinary market faster than the headline volumes suggest. Prices for standard memory have climbed, supply has tightened, and products with no connection to artificial intelligence have become more expensive because their components were conscripted into the AI build-out. A supercycle is what it looks like when one application becomes so valuable that it reorganizes an entire industry around its appetite, and the cost of that reorganization is paid by everyone else who needed the same factories. The AI accelerator does not just consume memory. It reprices memory for the world.

The Gate That Is Not in Taiwan

There is a strategic blind spot buried in this, and it is geographic. The whole anxiety about AI hardware concentration has been trained on Taiwan, and for the logic die and the CoWoS packaging that focus is correct. But the memory gate is not in Taiwan. It is overwhelmingly in South Korea, with SK Hynix and Samsung making the great majority of the world's HBM, and a single American maker, Micron, as the third. The most expensive, most sold-out, most physically demanding component in an AI accelerator comes from a different chokepoint than the one the maps are watching.

This widens the picture in a way that should be uncomfortable for anyone reasoning about resilience. There is not one chokepoint in AI hardware. There are at least three stacked on top of each other, the logic die and the packaging in Taiwan, the high-bandwidth memory in Korea, and each is concentrated in a handful of firms and a handful of buildings. A disruption to any one of them stops the others, because a logic die with no memory and no package is nothing, and HBM with no package and no die is nothing. The system everyone describes as a Taiwan risk is actually a chain of single points of failure spread across the Pacific, and the part most likely to bind first, the memory, sits in the country people are not even discussing. The visible risk stands in front of the structural one and hides it.

It Reaches Your Desktop

The clearest proof that this is a binding constraint and not an industry detail is that it has begun taxing ordinary people who have never bought an AI chip in their lives. Because HBM eats roughly triple the wafer capacity per gigabyte, and because the memory makers are diverting their best lines to it, ordinary computer memory has gone into shortage and its price has surged. The AI memory boom is, quite literally, eating the RAM in consumer machines, and the effects show up in places far from any data center. Even the dominant AI chip company reportedly planned to cut production of its own consumer graphics cards sharply in early 2026, because the memory those cards need was being consumed by the AI accelerators that pay more for it.

This is the signature of a true bottleneck. It does not stay politely inside its own market. It reaches outward and raises the price of everything that competes for the same scarce input, so that a student buying a laptop and a gamer buying a graphics card are quietly paying a tax levied by the AI build-out's hunger for memory. The constraint is not abstract and it is not distant. It is in the price of the thing on your desk, set by a shortage in a component most of those paying for it could not name.

Regulating the Wrong Layer

The clearest real-world proof that the spotlight is one layer too high is the shape of the export-control regime built to contain AI. It was written, first and most loudly, around the chip: restrict the most advanced logic processors, count them, license them, keep the leading dies out of rival hands. And for a while the policy and the public watched the same object, the processor, while the binding constraint sat untouched in the back end. A control regime aimed at the logic die is aimed at the part that is not, in supply terms, the scarcest, which is why the controls have since had to extend, belatedly and quietly, toward the things that actually gate production: high-bandwidth memory and the equipment that makes advanced packaging possible. The policy is migrating down the stack, chasing the constraint it originally missed.

That migration is itself the argument. If the chip were the true chokepoint, controlling the chip would have been sufficient, and there would have been no need to reach further down. The reaching is an implicit admission of where the gate really is. And it exposes the trap in the whole framing, which can be put as a single crossing: control the chip and you have controlled what is not scarce; leave the package free and you have freed what is. A strategy that fixes on the visible component will always be a step behind a system whose real limits live in the components no one campaigns about. The most consequential industrial constraint of the decade was legislated against at the wrong altitude, because the people writing the rules were watching the same object everyone else was, and the object was a decoy for the gate beneath it.

The Honest Objection

The strongest case against this reading is that the constraint is temporary and already being solved, and it deserves to be put at full strength. Capacity is being added at a furious pace. TSMC is roughly quadrupling CoWoS output. Competitors are arriving: Intel has its own advanced packaging technologies, EMIB and Foveros, that customers are now eyeing precisely because CoWoS is full, and Samsung and Micron are racing to expand HBM. Shortages, the objection runs, are how a market signals where to invest, and the enormous prices are summoning exactly the supply that will end them. Give it two or three years and the bottleneck eases, as bottlenecks usually do, and this whole analysis dates badly.

This objection is serious and partly right, and conceding it sharpens rather than weakens the point. Yes, capacity is being added, and yes, the specific shortage will eventually loosen. But notice what the concession does not touch. The capacity has already quadrupled and is still sold out, which means demand is outrunning even an extraordinary build-out, and a constraint that persists through a fourfold expansion is not a normal market wobble. More importantly, the structural fact survives the cyclical one. Even when this particular shortage eases, the production of AI hardware will still be gated by a small number of packaging lines and memory makers in a few buildings in two countries, and the bottleneck will not disappear so much as move, to the next least-substitutable step, or to the power and water and transformers that the finished accelerators then demand. The claim here is not that CoWoS will be scarce forever. It is that the determining variable in AI is always a concentrated physical step the conversation has not yet learned to watch, and that naming this one does not exhaust the pattern. It illustrates it.

The Spotlight Is Always Too High

This piece belongs to a set, and the set is the point. The transformer that cannot be built in time, the freshwater that cools the servers, the high-bandwidth memory that feeds the processors, the packaging line that assembles them: these are not separate stories. They are the same story told at different layers, the story of a civilization that believes it is building something weightless and keeps colliding with the most physical limits there are. In each case the public watches the glamorous object, the model, the chip, the data center, and in each case the binding constraint sits one layer down, in an unglamorous, concentrated, slow-to-build physical step that decides the outcome while the spotlight points elsewhere.

The lesson generalizes into a single discipline for reading any boom. Do not watch the breakthrough. Find the step beneath it that cannot be substituted, cannot be rushed, and is made in only a few places, and you have found the thing that actually sets the limit. In artificial intelligence the breakthrough is the model and the famous bottleneck is the chip, and both are misdirections, because the chip waits on a package the world cannot make fast enough and a memory it cannot make at all in the quantities required. The most advanced industry in history is rationed by its least visible step. We are counting processors while the future is being decided by an interposer and a stack of memory, in two countries, in a handful of rooms, by three or four companies whose names most of the people arguing about AI have never said out loud.

Evidence Map

Facts, interpretations, forecasts, and disconfirming signals.

Core claim. The binding constraint on AI hardware is not the logic die ("the chip") but two concentrated back-end steps: advanced packaging (TSMC's CoWoS) and high-bandwidth memory (HBM, made mostly by SK Hynix and Samsung in Korea, plus Micron). The public, the policy debate, and export controls remain fixed on the chip, one layer above the actual gate, which is the recurring mechanism by which a determining variable operates unseen.

Evidence level. Facts (high): CoWoS is TSMC's advanced-packaging process and is required to turn a logic die plus HBM into a shippable accelerator; TSMC has stated CoWoS is sold out through 2025 into 2026 and is scaling from ~35,000 to a projected ~130,000 wafers/month by end-2026 (~4x); Nvidia has reportedly secured 60%+ of CoWoS capacity for 2025-26; HBM is sold out, with SK Hynix (~50% share) citing sold-out status into at least Q4 2027, echoed by Samsung and Micron; HBM contract prices have roughly tripled since early 2024; HBM consumes ~3x the wafer capacity of standard DRAM per GB, pressuring consumer memory; Nvidia reportedly planned sharp consumer-GPU production cuts due to memory shortage; next-gen Nvidia hardware specs up to 288GB HBM. Interpretation (medium, marked): that packaging+memory, not the die, is now the determining variable; that the Korea memory gate is a strategically underwatched chokepoint; that the bottleneck migrates to the least-substitutable step. Forecast (speculative): that easing this shortage moves the bottleneck rather than removing it.

What would confirm this. Continued sold-out CoWoS and HBM despite capacity expansion; AI-driven consumer memory price surges; export-control regimes belatedly extending to packaging and HBM.

What would disprove this. Packaging and HBM capacity overtaking demand so that the logic die again becomes the sole binding constraint; or genuine diversification of HBM and advanced packaging across many firms and geographies, dissolving the chokepoint.

Watchlist. CoWoS capacity vs booking through 2027; HBM4 ramp and pricing; Intel EMIB/Foveros and other packaging entrants; DRAM prices as an indirect gauge; any export-control move targeting packaging or HBM rather than chips.