How IMF conditionality and investment treaties turned economic policy into permanent law

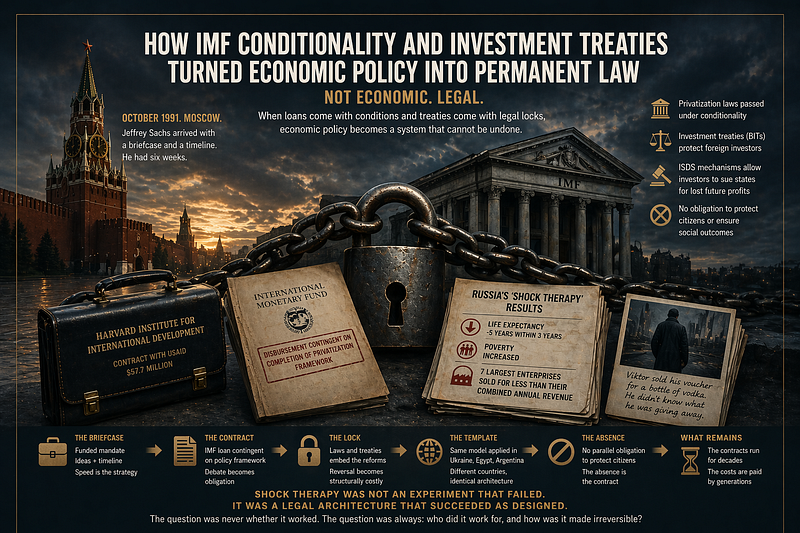

In the winter of 1991, a Harvard economist named Jeffrey Sachs boarded a plane to Moscow carrying a briefcase of policy recommendations. The Soviet Union had collapsed three weeks earlier. Russia had a new government, a devastated economy, and no functioning legal infrastructure for private ownership. Sachs had six weeks.

He called what he brought “shock therapy.” The name implied medicine: painful, temporary, necessary. What it actually contained was a legal architecture. And legal architectures do not expire.

The Briefcase

The recommendations Sachs carried were not improvised. They had been tested, first in Bolivia in 1985, then in Poland in 1989. In both cases, Sachs advised governments to move fast: liberalize prices, privatize state enterprises, open capital accounts, cut subsidies. He argued that reform needed to move “faster than any country has ever moved,” not as ambition, but as architectural necessity. Slower movement would allow opposition to consolidate.

The speed was not incidental. It was structural. A government that privatized rapidly created facts on the ground before democratic deliberation could catch up. By the time parliaments understood what had been transferred, the transfers were complete.

In Russia, the transfers moved faster than anywhere before. Between 1992 and 1994, state enterprises worth hundreds of billions of dollars were redistributed through a voucher system that most Russians did not understand and most could not use. What had been public infrastructure became private holdings, concentrated in the hands of a small number of men who became known as oligarchs. Seven banks, operating under rules designed by Western advisors, acquired controlling stakes in the country’s largest industries.

Viktor, a machinist in Nizhny Novgorod, received his voucher in late 1992. He exchanged it for shares in an enterprise he had worked in for eleven years. By 1995, those shares were worth less than the paper they were printed on. The enterprise had been acquired by a holding company he had never heard of. He was still employed. The building was the same. But the enterprise belonged to someone else now, and the contracts that made it so were governed by international investment law.

He did not know that. He was not supposed to know that.

The Contract

Jeffrey Sachs left Moscow in 1993. He later described his experience there as a failure, attributing it to insufficient Western financial support and to corruption within the Russian government. What he did not describe were the contracts.

Between 1992 and 1999, Russia signed a series of bilateral investment treaties with Western nations. These treaties were presented as protections for foreign investors, standard instruments of economic integration. What they actually created was a parallel legal system, one in which investment disputes could be adjudicated not by Russian courts but by international arbitration panels, outside Russian jurisdiction, under rules that Russian citizens had no vote in creating.

The architects of this system were not only Russian. The IMF attached conditionality requirements to its loans, requirements that included specific legal structures: private property protections, limits on renationalization, capital account liberalization. The World Bank followed similar frameworks. The legal infrastructure was not incidental to the financial assistance. It was the price of it.

By 1996, Russia had restructured its economy according to specifications written largely in Washington and Cambridge, Massachusetts. The specifications were binding. Not through force, but through law.

Mikhail Khodorkovsky, who had acquired Yukos Oil through the loans-for-shares scheme in 1995, understood the architecture better than most. When Vladimir Putin moved against him in 2003, Khodorkovsky’s lawyers argued before international arbitration panels, not Russian courts. In 2014, the Permanent Court of Arbitration in The Hague awarded Yukos shareholders $50 billion, the largest arbitration award in history.

The award was later annulled on jurisdictional grounds. But the mechanism that produced it remained. The contracts were still running.

The Lock

International investment law operates on a principle called the Fair and Equitable Treatment standard. Under this standard, a government that changes regulatory conditions in ways that affect investor expectations can be held liable for those changes, even if the changes are democratically enacted.

This is not a hypothetical. Between 1994 and 2014, more than 600 investment arbitration cases were filed globally. Governments were sued for raising minimum wages, strengthening environmental regulations, reversing privatizations that had proven damaging. The cases were heard not in national courts but in bodies like the International Centre for Settlement of Investment Disputes, an institution housed inside the World Bank.

The people who sat on arbitration panels were drawn largely from a small network of international law firms. They rotated between representing claimants and serving as arbitrators. There was no appeals process. Awards were final.

A legal system with no appeals process, staffed by rotating members of a small professional network, operating outside democratic oversight, adjudicating claims that constrain what elected governments can do: this is the architecture that shock therapy required to become permanent.

The lock was not metaphorical. It was procedural.

The Template

Russia was not the last country to receive this architecture. The same framework, adapted to local conditions, was applied across Eastern Europe, Sub-Saharan Africa, and Latin America through the 1990s and 2000s. Each application shared the same basic structure: rapid privatization, bilateral investment treaties, IMF conditionality, ISDS mechanisms.

The vocabulary shifted with each application. “Shock therapy” became “structural adjustment,” “structural adjustment” became “market liberalization”: each term describes a legal obligation in economic vocabulary. The underlying architecture did not change.

What changed was the sophistication of the delivery. By the time the same framework was applied to Ukraine’s agricultural land market in 2020, as a condition of a $5 billion IMF loan, the presentation was seamless. International financial integration. Modernization. Alignment with European standards.

The template had been refined over three decades. It no longer looked like a template.

The Absence

Jeffrey Sachs did not design the bilateral investment treaty system. He did not write the ISDS arbitration rules. He was an economic advisor, not a legal architect. This distinction is important.

It is also, in a precise sense, the mechanism.

The shock therapy framework created the conditions under which investment treaty law became necessary. Once privatization had occurred at speed, reversing it required compensating investors at market rates. Once capital accounts were open, closing them triggered treaty obligations. The economic recommendations and the legal architecture were not the same thing. But they required each other. One without the other would not have held.

Sachs later became a prominent critic of the Washington Consensus, of austerity, of the financial institutions whose frameworks he had helped implement. His criticism was genuine and often accurate. It did not engage the legal layer. It did not ask why the agreements signed during the reform period were still governing investment disputes thirty years later. It did not address what it means that a legal architecture installed in six weeks continues operating after the advisor who recommended it has changed his mind.

The contracts do not change their mind.

The law made it permanent. But the law was not the deepest layer.

The deepest layer was the assumption that legal permanence was not a political choice. That what was signed in 1992 simply was, the way mountains simply are. That the question of whether it should be revisited was not a legal question but an ideological one, and therefore not serious.

Viktor, in Nizhny Novgorod, was still an engineer. The enterprise was still owned by someone else. The contracts made both facts equally permanent.

That is the architecture. Not the briefcase. Not the economist. The contracts that kept running after everyone involved had moved on to something else.

The Manifest Archive publishes two versions of each analysis. This is the condensed version. The full text, including the complete ISDS legal architecture layer and the section on The Absence, is available on Substack. Free to read.

Related from The Manifest Archive